Chapter Three: Linear Regression

Applied problems

Load the Directories

BASE_DIR = os.path.dirname(os.path.dirname(os.path.abspath(__file__)))

DATA_DIR = os.path.join(BASE_DIR, 'Data')

IMAGE_DIR = os.path.join(os.path.join(BASE_DIR, 'Images'), 'Chapter3')

Problem 8

Part a) Simple Linear Regression

Load the 'auto' data

auto_df = pd.read_csv(os.path.join(DATA_DIR, 'auto.csv'))

As the horsepower column has some non numerical values we need to deal with them before any modelling.

auto_df['horsepower'] = pd.to_numeric(auto_df['horsepower'], errors='coerce')

auto_df['mpg'] = pd.to_numeric(auto_df['mpg'], errors='coerce')

auto_df.dropna(subset= ['horsepower', 'mpg',], inplace=True)

As we are concerned about the statistical significance of the predictor so we will use statsmodels rather than sklearn to construct the linear model.

## Set the target and predictors

X = auto_df['horsepower']

y = auto_df['mpg']

## Output statistical summary using statsmodels

results = smf.ols('mpg ~ horsepower', data=auto_df).fit()

The results of the simple linear fit are,

OLS Regression Results

==============================================================================

Dep. Variable: mpg R-squared: 0.606

Model: OLS Adj. R-squared: 0.605

Method: Least Squares F-statistic: 599.7

Date: Tue, 31 Mar 2020 Prob (F-statistic): 7.03e-81

Time: 10:22:20 Log-Likelihood: -1178.7

No. Observations: 392 AIC: 2361.

Df Residuals: 390 BIC: 2369.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 39.9359 0.717 55.660 0.000 38.525 41.347

horsepower -0.1578 0.006 -24.489 0.000 -0.171 -0.145

==============================================================================

Omnibus: 16.432 Durbin-Watson: 0.920

Prob(Omnibus): 0.000 Jarque-Bera (JB): 17.305

Skew: 0.492 Prob(JB): 0.000175

Kurtosis: 3.299 Cond. No. 322.

==============================================================================

From these results we can make the following conclusions:

i. There is a statistically significant relationship between the horsepower of a car and its mpg.

ii. The strength of the relationship is hard to quantify without other variables to compare to. What we can say is that, on average, an increase in one horsepower results in the decrese of 0.1578 mpg.

iii. There is a negative relationship between the horsepower and mpg (as expected.)

iv. Statsmodels linear plot conveniently produces the 95% confidence interval in the results. It is [-0.171, -0.145]mpg/hp.

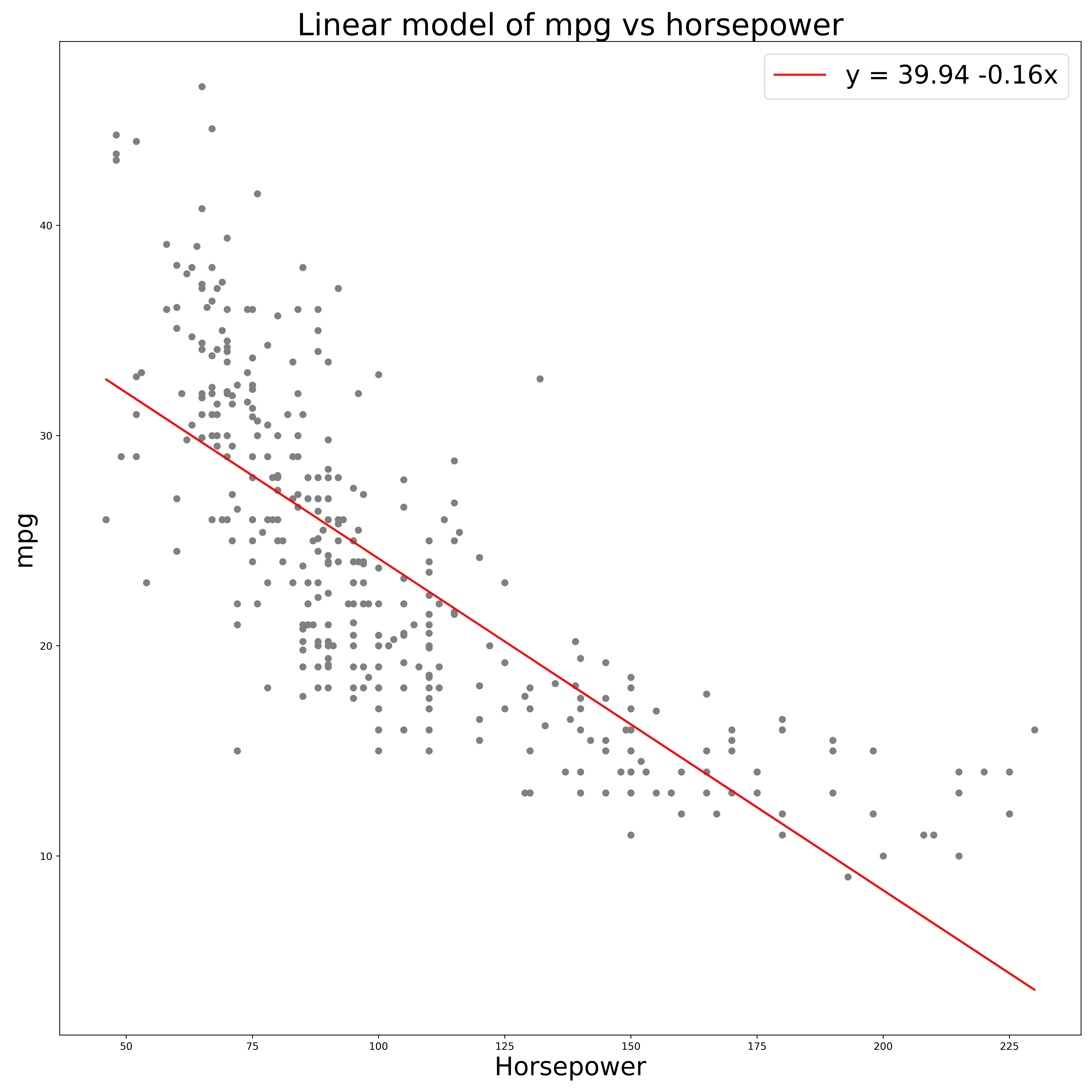

Part b) Linear plot

Using the python script for linear regression produces the following plot:

From this plot we can see the negative relationship between horsepower and mpg however it seems that a linear relationship is not the best fit. An exponential decay may be better. A relationship of the form,

$$ mpg = A\exp(-\beta*horsepower) + shift $$

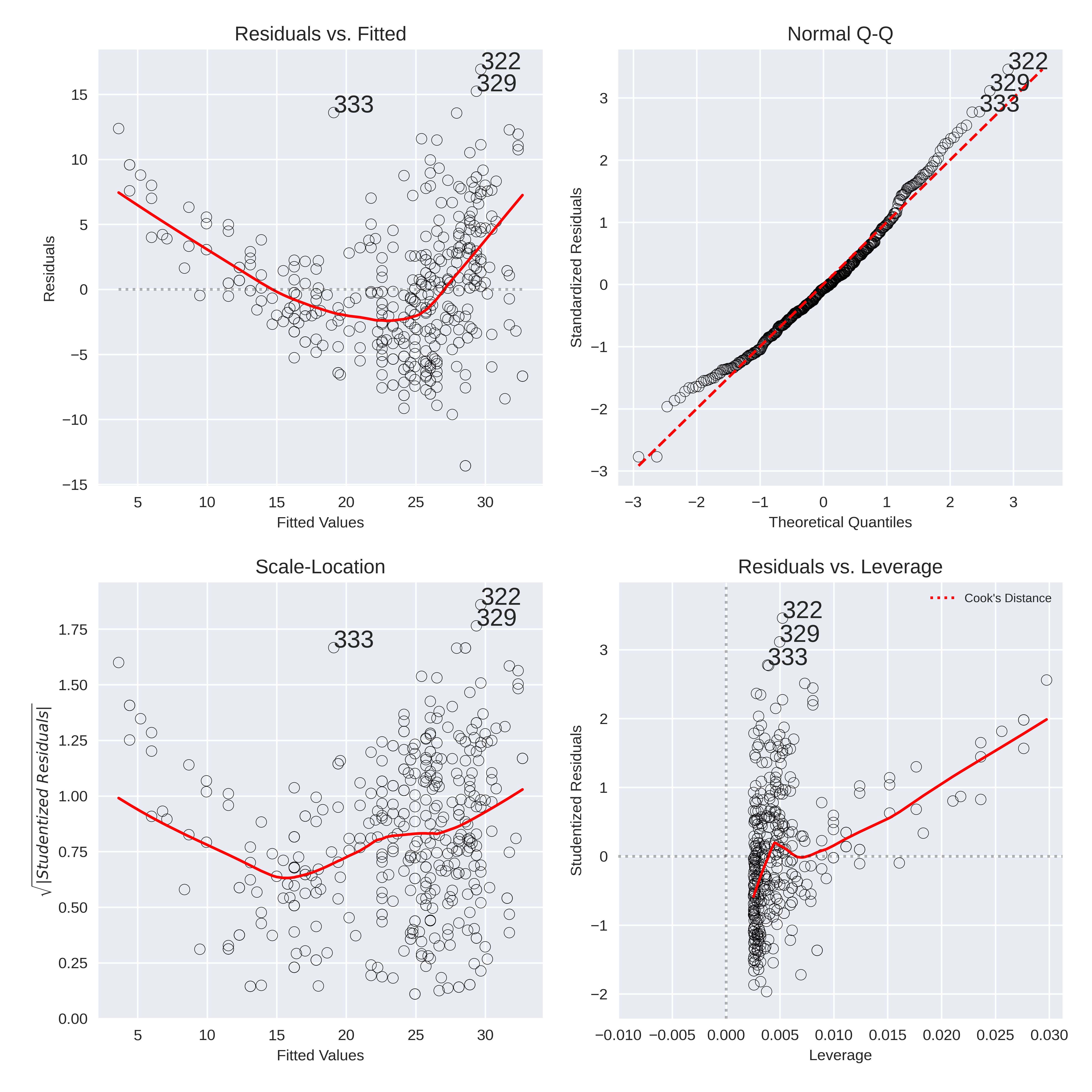

Part c) Diagnostic plots

The Diagnostic plots were generated with a python code from https://towardsdatascience.com/going-from-r-to-python-linear-regression-diagnostic-plots-144d1c4aa5a

The code is available in the acompanying script.

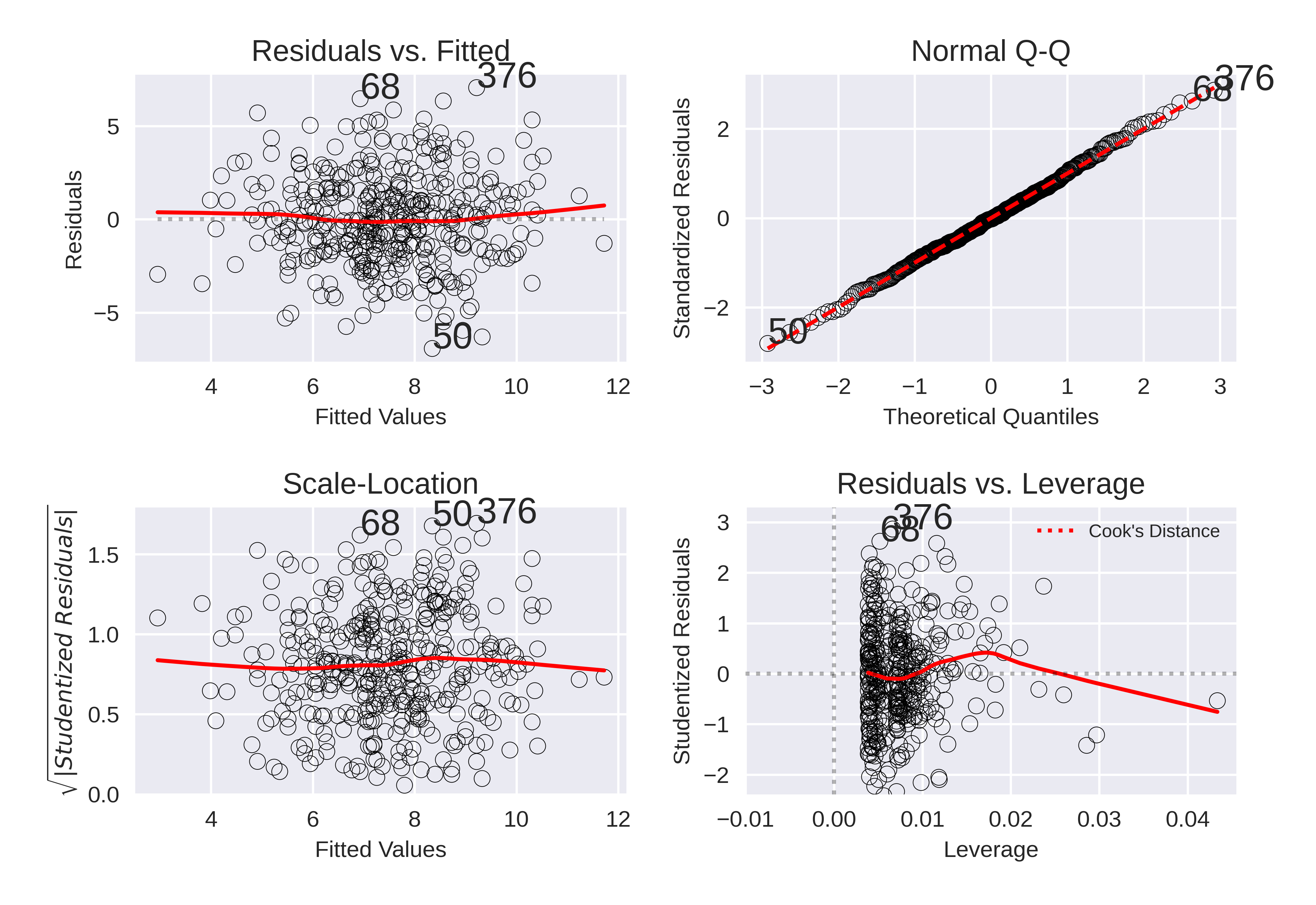

The Diagnostic plots of the simple linear fit above are:

From the diagnostic plots we see a few issues with the linear model:

Residuals vs. Fitted

- Ideally there should be no relationship between the residuals and the fitted values. However we see a clear trend, similar to a parabola. This may be due to the true relatinship being aexponential as discussed in the previous part.

Normal Q-Q

- The Normal Q-Q plot does not indictate a large degree of variing variance of the data which is a good signal.

Scale-Location

- THis is similar to the residuals plot and can tell us about the the heteroscedasticity (similar to the Q-Q plot). Here we can see that there is a degree of non-linearity and the varaince dows increase for the larger fitted values.

Leverage plot

- As there are no points outside the Cook's distance line (not even visible on the plot) we can confirm that there are no high leverage points to be discraded.

Outliers

From the Diagnostic plots we can see that there are some points which are consistent outliers. The most obvious outlier is point 333 which does not even follow the residual trend and should definitely be discarded. Two outher candidates are points 322 and 329. However, while these are outliers with the current regression they do lie in areas of out highly variant points. Therefore they might not be such significant outliers when using another combination of variables (For example, the exponential of the predictor).

Problem 9

SCRIPT: chap3_q9_script.py

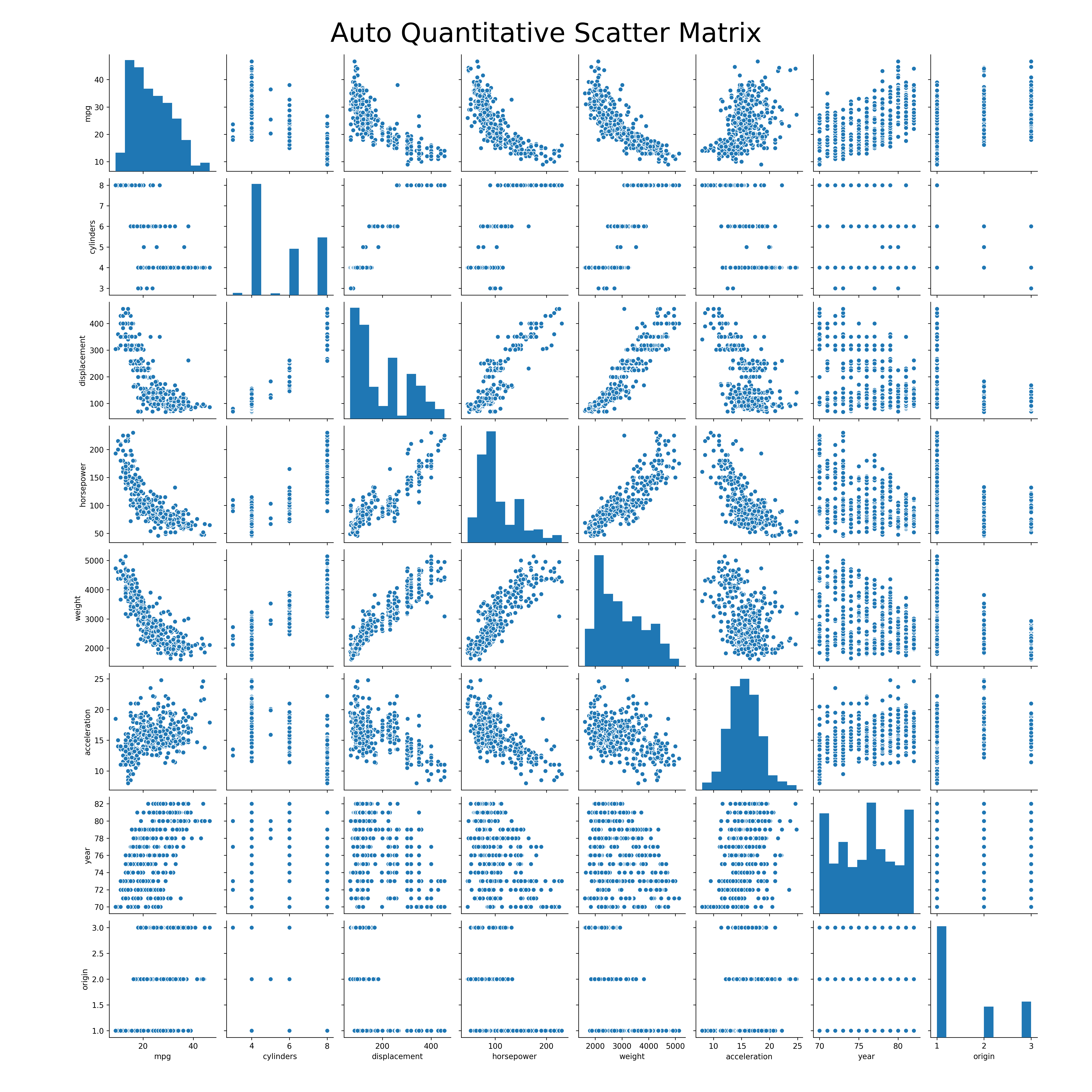

Part a) Scatter Matrix

Run the following code to generate the scatter matrix of all the variables.

auto_df['horsepower'] = pd.to_numeric(auto_df['horsepower'], errors='coerce')

auto_df['mpg'] = pd.to_numeric(auto_df['mpg'], errors='coerce')

auto_df.dropna(subset= ['horsepower', 'mpg',], inplace=True)

## Plot the scatter matrix

ax = sns.pairplot(auto_df)

plt.gcf().subplots_adjust(bottom=0.05, left=0.1, top=0.95, right=0.95)

ax.fig.suptitle('Auto Quantitative Scatter Matrix', fontsize=35)

plt.savefig(os.path.join(IMAGE_DIR,'auto_scatter_matrix.png'), format='png', dpi=250)

This produces the scatter matrix:

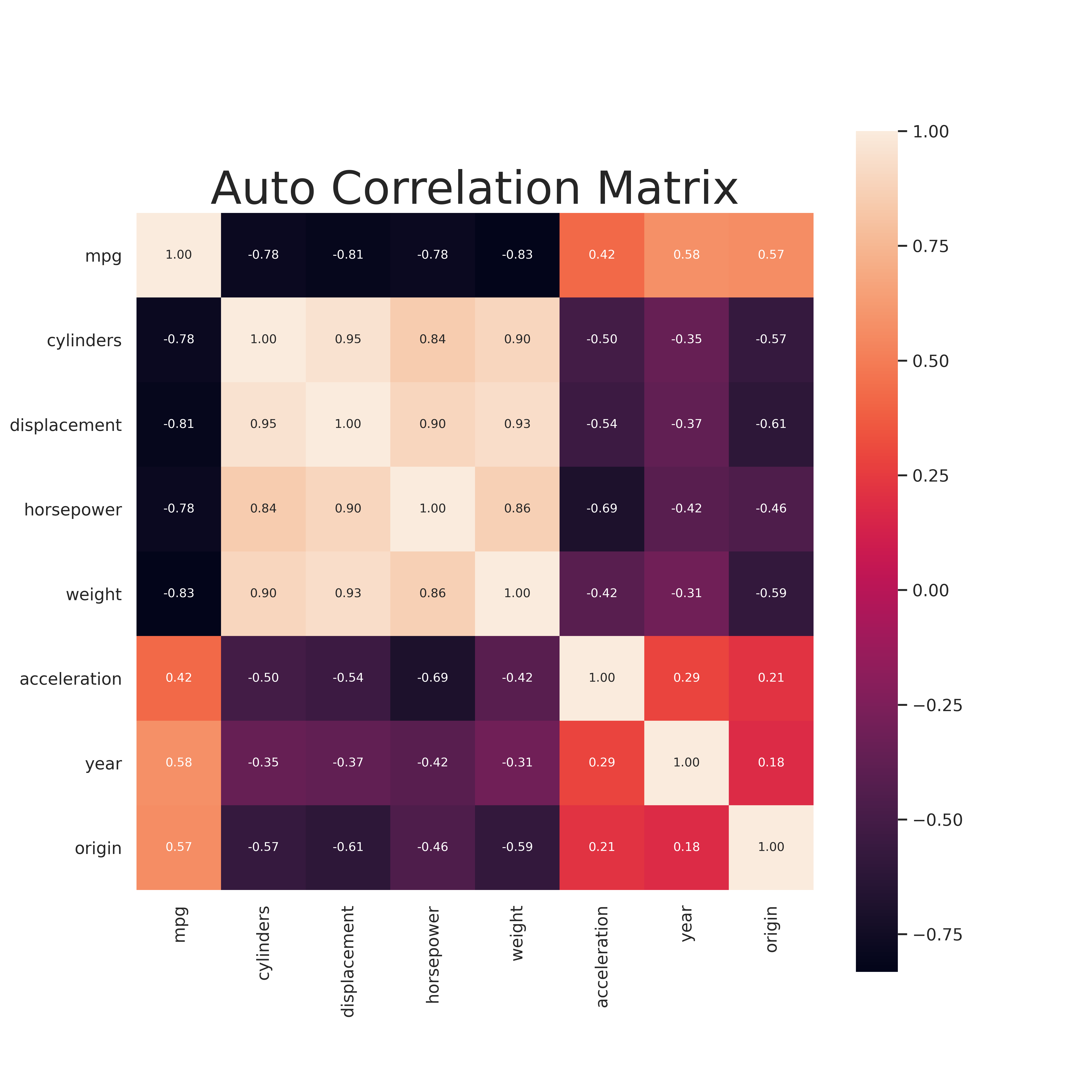

Part b) Correlation Matrix

Similar to above the following code generates the Correlation matrix for all the variables.

corr = auto_df.corr()

sns.set(font_scale=1)

fig, ax = plt.subplots(figsize=(10,10))

plt.title("Auto Correlation Matrix", fontsize=30)

hm = sns.heatmap(corr, cbar=True, annot=True, square=True, fmt='.2f', annot_kws={'size': 8}, ax=ax)

plt.savefig(os.path.join(IMAGE_DIR,'q9_auto_corr_matrix.png'), format='png', dpi=500)

plt.show()

Part c) Multiple Linear Regression

Now we perform multiple linear regression with most of the variable as predictors. The code is simply

## Create a string of features so we can use statsmodels.formula.api

feature_string = ' + '.join(X.columns)

## Fit the model

results = smf.ols("mpg ~ " + feature_string, data=auto_df).fit()

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: mpg R-squared: 0.821

Model: OLS Adj. R-squared: 0.818

Method: Least Squares F-statistic: 252.4

Date: Tue, 10 Mar 2020 Prob (F-statistic): 2.04e-139

Time: 12:42:00 Log-Likelihood: -1023.5

No. Observations: 392 AIC: 2063.

Df Residuals: 384 BIC: 2095.

Df Model: 7

Covariance Type: nonrobust

================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------

Intercept -17.2184 4.644 -3.707 0.000 -26.350 -8.087

cylinders -0.4934 0.323 -1.526 0.128 -1.129 0.142

displacement 0.0199 0.008 2.647 0.008 0.005 0.035

horsepower -0.0170 0.014 -1.230 0.220 -0.044 0.010

weight -0.0065 0.001 -9.929 0.000 -0.008 -0.005

acceleration 0.0806 0.099 0.815 0.415 -0.114 0.275

year 0.7508 0.051 14.729 0.000 0.651 0.851

origin 1.4261 0.278 5.127 0.000 0.879 1.973

==============================================================================

Omnibus: 31.906 Durbin-Watson: 1.309

Prob(Omnibus): 0.000 Jarque-Bera (JB): 53.100

Skew: 0.529 Prob(JB): 2.95e-12

Kurtosis: 4.460 Cond. No. 8.59e+04

==============================================================================

i. There is a relationship between the response and the predictors. The resulant linear model can explain 82.1% of the variance.

ii. The predictors with largest statistical significance are:

* displacement

* weight

* year

* origin

iii.* The coefficient for the year suggests a positive relationship between the year and mpg. This can be interpreted as more recently made cars have a high mpg. This is as we expect as newer cars are designed to be more efficient.

Part d) Diagnostic Plots

The Diagnostic plots are:

These diagnostic plots are promising in general. A few key points can be made: * There is no trend in the residuals compared to the fitted values. * The standardized residuals follow a normal distribution. * There are no obvious outliers. * There are no high leverage points.

Part e) Interaction effects

The following code includes interaction effects

## Create interaction effects with sklearn module

feature_names = X.columns

poly = PolynomialFeatures(interaction_only=True,include_bias = False)

X = poly.fit_transform(X)

## Create new linear model with new features

## Recreate dataframe out of preprocessed numpy array

column_names = poly.get_feature_names(input_features=feature_names)

columns = [name.replace(' ', '_') for name in column_names]

X = pd.DataFrame(data=X, columns=columns)

full_df = X.join(auto_df['mpg'])

feature_string = ' + '.join(columns)

formula = "mpg ~ " + feature_string

results = smf.ols("mpg ~ " + feature_string, data=full_df).fit()

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: mpg R-squared: 0.537

Model: OLS Adj. R-squared: 0.501

Method: Least Squares F-statistic: 14.85

Date: Tue, 31 Mar 2020 Prob (F-statistic): 1.98e-44

Time: 11:53:29 Log-Likelihood: -1192.3

No. Observations: 387 AIC: 2443.

Df Residuals: 358 BIC: 2557.

Df Model: 28

Covariance Type: nonrobust

=============================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------------------

Intercept -103.8187 110.244 -0.942 0.347 -320.625 112.988

cylinders -4.1160 16.869 -0.244 0.807 -37.291 29.059

displacement 0.0721 0.389 0.185 0.853 -0.694 0.838

horsepower 2.0423 0.709 2.882 0.004 0.648 3.436

weight -0.0720 0.037 -1.958 0.051 -0.144 0.000

acceleration 6.6092 4.449 1.485 0.138 -2.141 15.359

year 1.5100 1.264 1.195 0.233 -0.976 3.996

origin -7.0439 14.615 -0.482 0.630 -35.787 21.699

cylinders_displacement -0.0088 0.013 -0.669 0.504 -0.035 0.017

cylinders_horsepower 0.0426 0.049 0.864 0.388 -0.054 0.140

cylinders_weight -0.0015 0.002 -0.797 0.426 -0.005 0.002

cylinders_acceleration 0.1824 0.340 0.537 0.592 -0.486 0.851

cylinders_year 0.0399 0.199 0.200 0.841 -0.352 0.432

cylinders_origin 0.1183 1.017 0.116 0.907 -1.881 2.118

displacement_horsepower -0.0007 0.001 -1.210 0.227 -0.002 0.000

displacement_weight 6.836e-05 3e-05 2.276 0.023 9.3e-06 0.000

displacement_acceleration 0.0011 0.007 0.156 0.876 -0.012 0.014

displacement_year -0.0028 0.005 -0.575 0.566 -0.012 0.007

displacement_origin 0.0138 0.040 0.345 0.730 -0.065 0.092

horsepower_weight -9.751e-05 6.05e-05 -1.613 0.108 -0.000 2.14e-05

horsepower_acceleration -0.0149 0.008 -1.935 0.054 -0.030 0.000

horsepower_year -0.0203 0.008 -2.529 0.012 -0.036 -0.005

horsepower_origin -0.0790 0.061 -1.294 0.196 -0.199 0.041

weight_acceleration -9.463e-05 0.000 -0.201 0.841 -0.001 0.001

weight_year 0.0010 0.000 2.299 0.022 0.000 0.002

weight_origin 0.0012 0.003 0.349 0.728 -0.005 0.008

acceleration_year -0.0860 0.052 -1.646 0.101 -0.189 0.017

acceleration_origin 0.1474 0.319 0.462 0.645 -0.481 0.776

year_origin 0.0957 0.152 0.630 0.529 -0.203 0.394

==============================================================================

Omnibus: 2.593 Durbin-Watson: 1.271

Prob(Omnibus): 0.273 Jarque-Bera (JB): 2.414

Skew: 0.124 Prob(JB): 0.299

Kurtosis: 3.297 Cond. No. 3.82e+08

==============================================================================

The only two intereactions which appear to be statistically significant are: * displacement_weight * horsepower_year * horsepower_weight

The above model with all the interaction effects included is a poor model which cannot well explain the variance of the data.

Problem 10

Part a) Multiple Linear Regression

The following code fit the mulitple linear regress with predictors, Price, Urban and Us and response Sales

carseats_df = pd.read_csv(os.path.join(DATA_DIR, 'carseats.csv'))

carseats_df.drop('Unnamed: 0', axis=1, inplace=True)

### Fit the multiple linear regression

results = smf.ols("Sales ~ Price + Urban + US" , data=carseats_df).fit()

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Sales R-squared: 0.239

Model: OLS Adj. R-squared: 0.234

Method: Least Squares F-statistic: 41.52

Date: Sun, 15 Mar 2020 Prob (F-statistic): 2.39e-23

Time: 09:35:24 Log-Likelihood: -927.66

No. Observations: 400 AIC: 1863.

Df Residuals: 396 BIC: 1879.

Df Model: 3

Covariance Type: nonrobust

================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------

Intercept 13.0435 0.651 20.036 0.000 11.764 14.323

Urban[T.Yes] -0.0219 0.272 -0.081 0.936 -0.556 0.512

US[T.Yes] 1.2006 0.259 4.635 0.000 0.691 1.710

Price -0.0545 0.005 -10.389 0.000 -0.065 -0.044

==============================================================================

Omnibus: 0.676 Durbin-Watson: 1.912

Prob(Omnibus): 0.713 Jarque-Bera (JB): 0.758

Skew: 0.093 Prob(JB): 0.684

Kurtosis: 2.897 Cond. No. 628.

==============================================================================

Part b) Model interpretation

- Intercept: Self explanatory

- $\beta_{Price}$: For all other variables remaining constant, an increase in price of a single unit (dollar) results in an average decrease in unit sales of 0.0545.

- $\beta_{Urban}$: For all other variables remaining constant, an urban state will decrease the average sales by 0.0219. However this result is statistically insignificant.

- $\beta_{US}$: For all other variables remaining constant, a US state will increase the average sales by 1.2.

Part c) Equation form of model

The above move can be written as, $$ Y= \beta_{0} + \beta_{Price}X_{Price} + \beta_{US}X_{US} + \beta_{Urban}X_{Urban} $$

where $X_{i}=[0,1]$ for 'Yes' and 'No' respectively. This will result in 4 separate equations based on the values of the qualitative variables.

Part d) Rejection of Null Hypothesis

The Urban coefficient has a large P value and therefore is statistically insignificant.

Part e) New model without 'Urban'

Fit the New model with the following code,

carseats_df = pd.read_csv(os.path.join(DATA_DIR, 'carseats.csv'))

carseats_df.drop('Unnamed: 0', axis=1, inplace=True)

results = smf.ols("Sales ~ Price + US" , data=carseats_df).fit()

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Sales R-squared: 0.239

Model: OLS Adj. R-squared: 0.235

Method: Least Squares F-statistic: 62.43

Date: Sun, 15 Mar 2020 Prob (F-statistic): 2.66e-24

Time: 09:54:31 Log-Likelihood: -927.66

No. Observations: 400 AIC: 1861.

Df Residuals: 397 BIC: 1873.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 13.0308 0.631 20.652 0.000 11.790 14.271

US[T.Yes] 1.1996 0.258 4.641 0.000 0.692 1.708

Price -0.0545 0.005 -10.416 0.000 -0.065 -0.044

==============================================================================

Omnibus: 0.666 Durbin-Watson: 1.912

Prob(Omnibus): 0.717 Jarque-Bera (JB): 0.749

Skew: 0.092 Prob(JB): 0.688

Kurtosis: 2.895 Cond. No. 607.

==============================================================================

Part f) Model comparison

- Both models do not fit the data well at all based on the summary statistics.

- The low $R^2$ values suggest that there is a significant amount of unexplained variance in the moodels.

- The small value of the $F-$ statistic suggests there is not a significant relationship between the Price and the sets of predictors in either model. While the revised model is slightly better it is not sufficient to declare it a good model.

Part h) Diagnostic plots

The Diagnostic plots for the second model are:

From the plots we can conclude several things about the second model. * No outliers. From the Residual plots we can see that there are no significant outliers * No High Leverage Point: From the leverage plot there are no points outside of the cook lines and therefore- no points of hgh leverage. * Normal distribution of errors: From the residual QQ plot the residual errors follow a normal distribution. * heteroscedasticity: We see there is no trend in the absolute value of the residuals and therefore there is no trend in the error of the model.

This shows the nuances of linear regression modeling. Even with good diagnostic plots, the model can still be quite poor (low R squared value). Similarly, in problem 8 even though the diagnostic plots showed some issues, the R squared value was promising.

Problem 11

Part a) Linear regression with intercept

OLS Regression Results

=======================================================================================

Dep. Variable: y R-squared (uncentered): 0.814

Model: OLS Adj. R-squared (uncentered): 0.812

Method: Least Squares F-statistic: 434.3

Date: Sun, 15 Mar 2020 Prob (F-statistic): 5.57e-38

Time: 12:03:48 Log-Likelihood: -139.20

No. Observations: 100 AIC: 280.4

Df Residuals: 99 BIC: 283.0

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x 1.9162 0.092 20.840 0.000 1.734 2.099

==============================================================================

Omnibus: 0.147 Durbin-Watson: 1.908

Prob(Omnibus): 0.929 Jarque-Bera (JB): 0.014

Skew: -0.028 Prob(JB): 0.993

Kurtosis: 3.019 Cond. No. 1.00

==============================================================================

These results suggest (obviously) that the x coefficient is statistically significant. That is, $y$ is linearly dependent on $x$.

Part b) With intercept

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.802

Model: OLS Adj. R-squared: 0.800

Method: Least Squares F-statistic: 396.3

Date: Sun, 15 Mar 2020 Prob (F-statistic): 3.29e-36

Time: 11:54:30 Log-Likelihood: -138.14

No. Observations: 100 AIC: 280.3

Df Residuals: 98 BIC: 285.5

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -0.0110 0.098 -0.113 0.910 -0.205 0.183

x 1.8604 0.093 19.907 0.000 1.675 2.046

==============================================================================

Omnibus: 1.723 Durbin-Watson: 2.013

Prob(Omnibus): 0.422 Jarque-Bera (JB): 1.248

Skew: -0.005 Prob(JB): 0.536

Kurtosis: 3.547 Cond. No. 1.12

==============================================================================

We see that with an intercept the x-coefficient is still statistically significant as expected.

Part c) Model relationship

Both plots are very closely related. This is because the intercept, when included, is relatively small.